MN7060 Strategic Financial Management Assignment Sample

Explore How Ownership Structures and M&A Strategies Shape Strategic Financial Management Outcomes With Expert UK Assignment Help Today

- 92650+ Project Delivered

- 1500+ Experts 24x7 Online Help

- No AI Generated Content

- Introduction: MN7060 Strategic Financial Management Assignment

- Background and Context

- Aim and Objectives

- Scope and Relevance

- Literature Review

- Theoretical Background on Firm Ownership

- Theoretical Background on Mergers and Acquisitions (M&A)

- Theoretical Framework: M&A Related Theories and Their Relevance

- Analysis and Reflections

- Financing Structure and Its Role in M&A

- Relationship between Ownership Concentration and M&A Outcomes

- Dual Ownership and Its Impact on Returns and Voting Power in M&A

- Family Ownership and Acquisition Decisions

- Cross-Ownership and Its Influence on Corporate M&A Strategy

- Ownership Strategies in Cross-Border M&As

- Influence of Local Corruption on Ownership Strategy in M&As

- Overlapping Institutional Ownership in M&As

- Applicability of Weighted Average Cost of Capital (WACC) in M&A Decision-Making

Introduction: MN7060 Strategic Financial Management Assignment

Background and Context

M& A has been identified for several decades as an appropriate strategic concept for company development, restructuring and improving competitive positions. It can act as a value creating process when M&A helps certain companies to gain entry into a new market, acquire new technologies or gain volume required for economies of scale. Though such acquisition/ exits successful are not guaranteed. Some M&As deliver synergy and better financial outcomes while others are M&As failures ending in integration issues, cultural incompatibility or loss-making.

This essay will discuss that the ownership structure of the acquiring and target firms represents one of the key factors that determine the success or failure of the M&A transactions. Ownership structure is defined as the mix of stock ownership between one or more institutions, families and cross-share holding. The above ownership characteristics can impact on business decisions making process, risk tolerance, and long-term organizational goals and objectives that determine the outcomes of M&As.

Assignment deadlines piling up? Let New Assignment Help ease your burden with expert Assignment Help UK tailored for student success.

Aim and Objectives

The more specific aim of this report are to: explore the dynamics of firm ownership structures and answer the question: ‘To what extent does firm ownership influence M&A performance?’ Specifically, it focuses on the following objectives:

- To understand how concentrated ownership structure and family ownership affects M&A decisions and whether cross-ownership and institutional ownership would positively influence M&A performance of firms.

- To examine the impact of ownership characteristics on the subsequent post change integration, governance and financial performance.

- To compare the strategic fit and culture of organisations according to their ownership structure in order to test hypothesis two.

Criticizing the prior research and empirical investigation, the report will identify how ownership structure may contribute positively or negatively towards the achievement of M&A operations.

Scope and Relevance

The evidence used in the study encompasses both developed and emerging economies, thereby providing a rich perspective on the ownership-M&A relationship in various conditions in global economies. While the structure of EMs is quite different in terms of concentrated ownership, family firms, M&A related issues possess different prospects and challenges exams (Candra, et al. 2021). By contrast, the M&A activity in developed markets, as has already been postulated, might be characterised by a stronger institutional ownership and regulation impact on, and a consequent dissimilar effect upon, the M&A strategies of the firms.

Strategic financial management assignments require deep understanding of corporate valuation and risk; accessing expert finance assignment help ensures students apply appropriate financial models with precision.

The following dynamics are explored and prospective best practices are proposed for actions across different ownership regimes in this report to enhance M&A for policymakers and others, such as CEOs and investors involved in numerous ventures. Therefore, comprehending on how ownership structure negotiates with M&A performance is critical towards optimising value creation and risk management in corporate deals.

Literature Review

Theoretical Background on Firm Ownership

- The firm ownership structure is discovered to significantly influence corporate governance, strategic management and, consequently the outcomes of M&A (Chen, et al. 2020). The ownership structures are; concentrated ownership, family ownership, institutional cross-ownership and dual ownership, and each has its feature and ramifications.

- Concentrated ownership means a situation where a large number of stocks in a company are owned by a handful of stockholders (Degbey, et al. 2021). This includes the major investors or founders of the companies who remain the major decision makers of important issues such as M&As.

- Family ownership is highly evident in many firms most especially in the emerging markets. In this type of firms, there is always a strong tendency that family members are appointed to top managerial posts and retain decision-making powers on corporate matters (Santulli, et al. 2022). Bureaucratic structures are often associated with long term horizons and risk avoiding behaviours which are NOT insurmoutable when it comes to M&A decisions.

- Institutional cross-ownership occasionally includes several companies in the same sector being controlled by large companies like mutual funds or pension funds (Zhu, et al. 2024). While this structure might be likely to involve the company in conflicts of interest situations, it is also likely to encourage synergy strategies and minimize competitiveness.

- Dual ownership is a term used when the control of the assets and the management of the company are in different hands, the shareholders’ control the voting rights. This structure results in agency problems, as described under agency theory, as distinguish the divergence of interest between the owners, who are the principals, and the managers, who are the agents (García, and Herrero, 2022). Agency theory offers a framework with which it is possible to understand the consequences of varying structures of ownership in M&As and their performance and governance.

Theoretical Background on Mergers and Acquisitions (M&A)

Mergers and acquisitions, M&A, refer to corporate amalgamation activities involving two or more companies joining to become one firm or a buyer firm absorbing another firm. M&A transactions can be classified into three primary types based on the relationship between the merging firms:

- Horizontal Mergers: These are usually between firms in the same trade, and frequently within the same league, as it were (Suryaningrum, et al. 2023). The first organizational objective is the push up the amount of market share, the lessening of competition and the utilization of substantial scales.

- Vertical Mergers: These are the ones that happen between firms at different levels of the same supply chain whereby one firm merges with another supply chain provider (Rani, et al. 2020). The aim is to optimize operation output, minimize cost of transactions, and increase supply chain management.

- Conglomerate Mergers: These are cross industry ventures intended at managing business risks and venturing into new lines of business (Mbuthia, et al. 2021).

- The most common managerial motives for M&A are: “synergy” operating cost or increased revenues, “increasing market presence” by a geographical presence or customers’ base and the “acquisition of valuable resources” like technology, people and knowledge.

Theoretical Framework: M&A Related Theories and Their Relevance

- Agency Theory: Agency theory is useful in depicting relationship between ownership structure and M&A. They worked to expose the self-interested shenanigans of principals (owners) and agents (managers) when the self-interests are different. Agency costs are lower in concentrated or family ownership since managers are monitored closely thereby observing higher value adding M&A decisions (Al-Faryan, 2024). On the other hand, dispersed ownership might exacerbate the agency issues as institutional shareholders might not fully control the operation of the firms; thus, promoting value-reducing acquisitions due to managerial egocentricity.

- Resource-Based Theory: Furthermore, the resource-based theory highlights strategy fit in M&A evaluation for improving competitive advantage gained from resources. Transaction cost theory postulates that choice of ownership structures affects the efficiency of integration decisions, which reduce the cost of opportunism and contractual hazards (Jiang, et al. 2023). Taken together, these theories offer the basis within which we can examine the effects of ownership types on M&A performance, and reveal important performance differences resulting from different ownership structures.

- Empirical Evidence on Ownership and M&A Performance: Qualtitative analyses of the literature have equally disclosed the sides of ownership structures relative to M&A performance with the hope of understanding how different ownership shapes up the performance and strategic direction of M&As.

- According to, Bhaumik, and Selarka, 2012: the study examined the effect of the extent of the domination of corporate ownership on M&A performance in emerging economies, notably India. They found out that following the merger, firms with closer and concentrated ownership structure involving large stockholders or founding families post better results. This can be explained by the facts that dominant shareholders have a tight control on the corporative management and have less agency costs, so their decisions reflect shareholders’ interests more effectively.

- According to, Caprio et al. 2011: the research focused on the experience of family ownership in the acquisition process. Their research suggests that family controlled companies are more risk averse in acquisitive activities focusing on organic development instead of quick profits. The study established that family ownership impacted selection of target firms was obtained from the establishment and this was because the family favoured those that fit the family’s vision and tendency towards risk, and although this reduce risk it might also limit growth prospects were also more likely to be acquired by the family firm.

- According to, Brooks et al. 2018: the research looked at institutional interlocking which involves situations where the same institutional investors have stakes in several different companies in the same industry. They insisted that their study pointed to the fact that cross-ownership hampers competition and fosters cartel like behaviour in M&A deals. But it also creates some opportunities of conflict of interest because institutional investors may have a combined performance of stocks rather than the specific firm performance.

- According to, Goranova et al. 2010: their anlysis concerns with the area that categorized by six different forms of synergy, especially twofold share ownership, which is a kind of institutional share ownership where the same institutional investors are involved in acquiring and target firms.

It also found that overlap is likely to enable more efficient M&As by eliminating or lessening conflicts and animosities over the bargaining processes between the two firms. But this can also result in lower acquirer analyst following, weak post-acquisition management, and could have an impact on long term performance.

These empirical findings highlighted that ownership structure is highly relevant and crucial for understanding of M&A and how different types of ownerships impact across the strategic management, boards of directors and post merger performance.

Analysis and Reflections

- Definitions of Ownership Structures in M&A : Ownership structures play a pivotal role in shaping M&A strategies and outcomes:

- Concentrated Ownership: It will recall as a situation where one or many individuals own a large number of stocks in business, thereby making more decisions regarding the stocks.

- Family Ownership: It is a model where a family holds a significant share in the company and concentration on the sustainability of their family business.

- Institutional Ownership: It contains investors such as the pension funds or mutual funds, which exercise shareholders control over companies.

- Dual Ownership: It arises when two or more organizations have a large proportion of ownership stakes in each other, making them affect each other’s voting rights and other policy making decisions during M&A transactions.

Financing Structure and Its Role in M&A

The source of funding has therefore been found to impact the M&A transactions and the resulting results of such transactions. Acquisitions can be financed by debt, equity or a mixture of both and the effect on the firm’s capital structure and risk will differ. The use of debt financing is a taxed favourable while it incurs financial risk and leverage which implies that it to firms with stable cash flow. Equity financing reduces ownership, but has less financial risk than debt financing. Location of funds affects the integration or the acquisition and the post-acquisition integration in relation to cost of capital and wealth of shareholders hence is will appropriate as a significant parameter in M&A decisions.

Relationship between Ownership Concentration and M&A Outcomes

Evidences also depict that high concentration of share ownership can be extremely influential on M&A performance, especially in the emerging market atmosphere. Bhaumik, and Selarka, 2012 offer a theoretical prediction of the positive effect of concentrated ownership in post-merger performance and present relevant evidence from the Indian context, pointing out that agency costs determine this relationship. Signs of ownership concentration include having a big ownership stake by managers, big shareholders like founding families or institutions, which reduces contract risk because managers cannot pursue their self interests. This oversight makes certain that the acquisitions and mergers taking place within the firm are strategic for the organization thus proper resource utilization to boost post-acquisition performance.

Nevertheless, concentrated ownership carries its problems with it. Sometimes the large shareholders will act in their best self interest as opposed to the overall interest of the entire firm especially the minority shareholders. Furthermore, in markets, where the legal protection is somewhat less rigorous, concentrated ownership is likely to worsen governance issues, including tunnelling or the expropriation of minority shareholders.

Also, the evidence reported by Nogueira, and Kabbach de Castro, 2020, concluded that M&A performance can positively enhance through the concentrated ownership however the effectiveness of such ownership depends on the institutional surroundings and its related governance system that provides so far minority shareholders. concentrated ownership may hurt governance but is less likely to do so where legal standards are weaker. This is the reason regulation plays an important role in preventing inequality between investors or shareholders and others in emerging markets

Dual Ownership and Its Impact on Returns and Voting Power in M&A

When there is duality of share control through the holding of voting and non-voting shares large scale acquisitions and mergers may be strongly impacted by financial returns and voting power. Bodnaruk, and Rossi, 2016, case motivates us to study this pattern and discover that having two layers of shareholders with different levels of authority usually results in concentrated voting rights, which allow the controlling investor to manage the firm without bearing much risk. It provides the possibility for a majority of shareholders to implement strategic management in M&As that are most suitable for achieving the overall strategy envisioned by the whole company, even if these strategies may be less suitable for minorities.

Portfolio considerations also detail the effect of mass ownership on M&A returns with mostly moderate impacts. On the one hand, the mentioned control over the voting rights can stimulateMthe adoption of clear strategic initiatives, for example, acquisition of attractive targets or expansion to new fields that are likely to increase the value added in the long term. At the same time, controlling shareholders’oligopolistic power, on the one hand, can result in the decision making that is inefficient including acquiring targets at overvalued prices or implementing strategies in the shareholders’interests rather than the firm’sprofitability.

Also, according to Lewellen, and Lowry, 2021, the incessant clash of interest arise from the fact that dual-operation leads to the control share being a proper of controlling shareholders. This divergence is often likely to lead to lower value for shareholders especially where M&A decisions remain beyond the purview of independent directors or external investors. Litigation and regulation, shareholder activism in particular, are the most important factors in portraying the common risks of dual ownership in M&A deals.

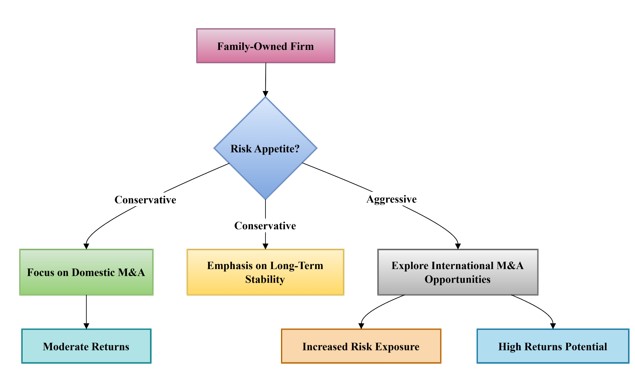

Family Ownership and Acquisition Decisions

Some of the remarkable features of family business when it comes to M&A strategic directions are the main features of family business ownership, survival, and control objectives and other mitigation factors that hedge the family business M&A strategies. Caprio et al. 2011 Looking at the impact of family ownership, this paper explores the impact of FOK on acquisition and discovers that FOFs use a defensive approach to M&A. These firms are unlikely to embark on risky acquisitions compared to their strategic objectives to maintain financial balance and continuing a family’s lineage.

Figure 1: Risk Appetite and Acquisition Strategies for Family Ownership

The research also found that the political dependent variable of the ‘conservative’ firms has a neutral effect on the M&A performance, since this characteristic of the family-owned firms can work as an advantage and disadvantage at the same time. There are positive effects as well, such as, focusing on risk management and the long-term stability would mean that there are decreased probability of engaging in activities that lead to value-destructive acquisition decisions. Third, there is heightened acquisition of suitable and compatible candidates, and the post-acquisition integration of targeted firms, by family business enterprises can also be explained by the fact that the acquirers are often also parent firms which strengthens the consolidated entity and provides post-acquisition synergistic benefits to the ex swimmer firm. However, the conservative style can also sometimes avoid growth prospects, since high-growth but high-risk businesses, which may create excellent value for shareholders of the acquiring firm, may not be considered by family-controlled businesses. The authors also affirm that M&A direction in family enterprises depends on the relationship between risk management and growth, and this can be addressed by the professionalization of the management and the diversification of ownership.

Cross-Ownership and Its Influence on Corporate M&A Strategy

This study established that corporate M&A strategies are influenced by institutional cross-ownership, a situation in which institutional investors invest in different firms within the same industry. Brooks et al. 2018 investigate the cross-ownership in a strategic context and discovered that it is likely to encourage cooperativeness among firms, thus leading to less rivalry and industry consolidation. Cross-ownership involves the ownership of stakes by one firm in other related firms rather than different unrelated firms, thus institutional investors have at stake the operational performance of the whole portfolio and not a single firm.

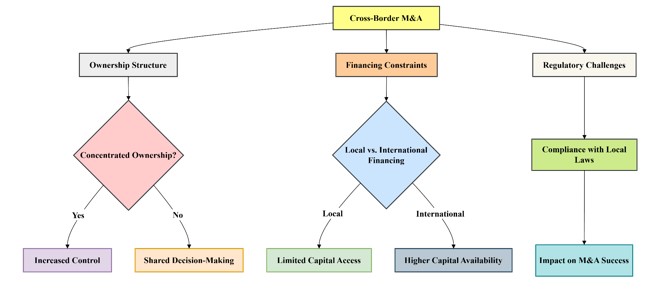

Figure 2: Ownership Strategies in Cross-border

Cross ownership increases this probability of cooperative M&A strategies like joint venture, strategic alliance and friendly merger, all, which bring more stability and better returns in the health care industry. Nonetheless, the integration points here also have their difficulties, especially when potential conflicts of interest arise on cross-ownership. It has been pointed out that institutional investors may act with an eye on a particular portfolio’s figures as a whole rather than focusing on the best course of action for each company in which they invest, therefore they can make decisions that are not in the best interest of shareholders of all the institutions involved. According to the authors, cross-ownership diminishes the abilities of markets to counter anti-competitive behavior they think can lead to a decrease in the rate of innovation. To redress these issues, cross-ownership and related concerns need to be regulatively limited and ownership information have to be made to be more transparent to prevent cross-ownership from disturbing the working of competitive markets and shareholders’ rights.

Ownership Strategies in Cross-Border M&As

The first limitation is that cross border M&As were always faced with some challenges some of which include the financial constraints and ownership control. Chen et al. (2009) analyse cross-border M&As in East Asian economies and stress the point that firms in these areas may have severe financing obstacles while completing acquisitions of overseas companies. To address these realties, the firms ensure that the ownership strategies adopted allow maximum control of the business, and minimum financial exposure. For example, when East Asian firms acquire 50 percent plus one share they are able to control the management of the acquisition target in a manner that corrects the worry of cultural and regulatory disparities from the intended strategy. The authors also stress that a significant financial support and government endorsement was needed to enhance the cross border acquisitions.

Influence of Local Corruption on Ownership Strategy in M&As

Cross border M&A deals’ ownership strategies are still greatly determined by local corruption. Di Guardo et al. (2016) show that when businesses venture into countries with corrupt markets they employ joint ventures or minority stakes to manage on risks resulting from ambiguous regulations and bribery pressures. It minimises one’s interaction with corrupt practices while at the same time benefited from the local partners’ knowledge and acquaintances. Nonetheless, corruption belongs to the causes that repel the foreign investors discussing the necessity of anti-corruption activities and appropriating due diligence checks in M&As with the overseas targets.

Overlapping Institutional Ownership in M&As

Goranova et al. (2010) focusing on the prevalence of multiple overlaps where more than one institutional investor has an interest in both the acquiring and target companies. This overlap can decrease rivalry and foster collaborative M& pace thus minimizing problems of negotiating and integrating M&A deals. But it may also lead to agency cost, as institutional investor’s primary objective is the portfolio level performance rather than the value of individual firms. The authors also claim that multiple business relations between the firms involved can positively affect the M&A performance if the acquirer and/or the target firm disclose all the related interests and cooperate on managing the conflict of interest [Referred to Appendix 2].

Applicability of Weighted Average Cost of Capital (WACC) in M&A Decision-Making

The Weighted Average Cost of Capital (WACC) is seen as an important diagnostic approach when it comes to mergers and acquisitions. It is a weighted average of the cost of equity and the cost of debt giving a clue of a firm’s required return rate. In M&A, WACC is useful in approximation of the target firm to determine if the expected returns can justified the cost of capital. A lower WACC reflects more favourable financing conditions, Therefore, acquirer’s WACC improves the ability to achieve synergy (Dobrowolski, et al. 2022). Although, its relevance is not fixed within industries and markets, therefore, sensitivity analysis should be implemented when making decisions and controlling risks in M&A processes.

Conclusion

Summary of Key Findings

In this essay, various ownership structures have been discussed; and the impact of these structures on mergers and acquisitions (M&A) has also been understood. Concentrated ownership generally provides better control and decision making especially so in emerging economies while on the other hand firms with family ownership tend to be set in their ways and avoid over expansion. This report examines how dual ownership affects both returns and voting rights and in particular how it may lead to conflict between shareholders. While institutional cross-ownership can promote synergistic relations, it necessarily leads to a conflict of interest situation. Finally, multiple Shareholder’s Syndrome promotes the cooperation in M&A activities, though it envisages the conflicts of interests need strict barrier.

Implications for Practice

In M&A exercises, firms should consider their ownership structure to formulate the type of strategies to undertake. For instance, family firmed needs to think about their capabilities regarding risk appetite while companies that experience institutional cross ownership needs to have stakeholder centrality. Improving the effective governance and increasing the M&A related investment while performing proper legal study in relation to all types of M&A ownership is crucial.

Limitations and Future Research

Current research is somewhat narrow in terms of geography and industry, which makes the applicability of the results rather questionable. Subsequent research should focus on the relationship between ownership structures and future trends of M&A around the world especially in the digital and emerging markets.

Reference List

Journals

- Al-Faryan, M.A.S., 2024. Agency theory, corporate governance and corruption: an integrative literature review approach. Cogent Social Sciences, 10(1), p.2337893.

- Bhaumik, S.K. and Selarka, E., 2012. Does ownership concentration improve M&A outcomes in emerging markets? Evidence from India. Journal of Corporate Finance, 18(4), pp.717-726.

- Bodnaruk, A. and Rossi, M., 2016. Dual ownership, returns, and voting in mergers. Journal of Financial Economics, 120(1), pp.58-80.

- Brooks, C., Chen, Z. and Zeng, Y., 2018. Institutional cross-ownership and corporate strategy: The case of mergers and acquisitions. Journal of Corporate Finance, 48, pp.187-216.

- Candra, A., Priyarsono, D.S., Zulbainarni, N. and Sembel, R., 2021. Literature review on merger and acquisition (Theories and previous studies). Studies of Applied Economics, 39(4).

- Caprio, L., Croci, E. and Del Giudice, A., 2011. Ownership structure, family control, and acquisition decisions. Journal of Corporate Finance, 17(5), pp.1636-1657.

- Chen, J., Zhao, X., Niu, X., Fan, Y.H. and Taylor, G., 2020. Does M&A financing affect firm performance under different ownership types?. Sustainability, 12(8), p.3078.

- Chen, Y.R., Huang, Y.L. and Chen, C.N., 2009. Financing constraints, ownership control, and cross‐border M&As: evidence from Nine East Asian economies. Corporate Governance: An International Review, 17(6), pp.665-680.

- Degbey, W.Y., Rodgers, P., Kromah, M.D. and Weber, Y., 2021. The impact of psychological ownership on employee retention in mergers and acquisitions. Human Resource Management Review, 31(3), p.100745.

- Di Guardo, M.C., Marrocu, E. and Paci, R., 2016. The effect of local corruption on ownership strategy in cross-border mergers and acquisitions. Journal of Business Research, 69(10), pp.4225-4241.

- Dobrowolski, Z., Drozdowski, G., Panait, M. and Apostu, S.A., 2022. The weighted average cost of capital and its universality in crisis times: Evidence from the energy sector. Energies, 15(18), p.6655.