SOE11146 Business Economics Finance Global Environment Assignment Sample

Get Expert SOE11146 Business Economics and Finance in a Global Environment Assignment Help from Top UK Academic Writers Today!

- 92650+ Project Delivered

- 1500+ Experts 24x7 Online Help

- No AI Generated Content

- 1: Introduction Of Business Economics And Finance Global Environment Assignment

- 2: Investment Appraisal Approach

- 2.1: Net Present Value (NPV)

- 2.2: Internal Rate of Return (IRR)

- 2.3: Payback Period (PBP)

- 2.4: Profitability Index (PI)

- 3: Investment Appraisal Analysis

- 3.1: Assumptions

- 3.2: Net Present Value

- 3.3: Internal Rate of Return

- 3.4: Payback Period

- 3.5: Profitability Index

- 4: Budgeting Approach for Clark Casc Logistics Plc

- 4.1: Integration from Top and from Bottom

- 4.2: Activity Based Budgeting (ABB)

- 4.3: Rolling Budgets

- 4.4: Scenario Planning

- 4.5: The Performance Observation and Metrics

- 5: Budgeting Calculations and Analysis

- 5.1: Assumptions

- 5.2: Sales Budget

- 5.3: Salaries and Payroll Cost Budget

- 5.4: Property, Plant and Equipment Budget

- 5.5: Building Depreciation and Maintenance Budget

- 5.6: Vehicle Cost and Other Equipment Budget

- 5.7: Vehicle Fuel, Staff Training and Step Fixed Cost Budget

- 5.8: Proposed Income and Expenditure Budget

1: Introduction Of Business Economics And Finance Global Environment Assignment

This report focuses on the importance of business economics and finance in Global economics. Firstly, it discusses investment appraisal approaches like NPV, IRR, PBP and PI. Secondly it focuses on investment appraisal analysis of the different approaches, assumptions and overall recommendations. Thirdly, the budgeting approaches of Clark Casc Logistics Plc which are integration from top and from bottom, activity-based budgeting, rolling budgets, scenario planning and the performance observation and metrics. Moreover, this report will discuss the budgeting calculations and different analyses like budget sales budget, salaries and payroll cost budget, property, plant and equipment budget, building depreciation and maintenance budget, vehicle fuel, staff training and step fixed cost budget and proposed income and expenditure budget. And lastly, conclusions and recommendations.

Students studying business economics and finance in a global environment often need expert accounting assignment help UK to tackle complex financial reporting and analysis tasks confidently.

2: Investment Appraisal Approach

For Clark Casc Logistics Plc (CCL) , financial measures are among the key instruments for the assessment of investments. This aspect is quite useful in that it makes the decision regarding distribution of resources, and capital investment more informed (Baum, Crosby & Devaney, 2021).

2.1: Net Present Value (NPV)

NPV is widely used at CCL because it helps the company determine the actual difference between the current value of cash inflows and cash outflows over the project’s lifespan. The NPV equals or is higher than zero if the project cost of capital is expected to generate more than the cost of capital, thus being profitable. Having an exact figure for the correct discount rate, NPV enables CCL to allocate resources to those initiatives that will have the most lasting positive impacts on its business (Peymankar, Davari & Ranjbar, 2021).

2.2: Internal Rate of Return (IRR)

IRR is another useful financial ratio that is used in determining the potential of investment. It defines how rapidly a project’s NPV becomes zero. Company’s investment evaluation criteria to determine the projects with maximum potential includes an IRR greater than the company required rate of return. According to CCL, IRR may be used to compare several investment operations and select which ones can be profitable according to their financial goals.

2.3: Payback Period (PBP)

The payback period is a tool that calculates durations it takes to get back an initial investment through cash receipts. Straightforward and it raises liquidity issues and project risks. CCL mentioned that shorter PBP prevails, more so for investments made in volatile industries that require quick returns for firms in the evolving logistics industry (Imteaz, Bayatvarkeshi & Karim, 2021).

2.4: Profitability Index (PI)

This is used in the context of using different kinds of present value amounts of probable future earnings, although it is previously known as the measure of probable profitability to divide the present worth of future earnings to the value of an initial investment. Again, a PI more than one is an indication of a financially viable project. For CCL this is useful when comparing many different projects, where it allows one to determine which to embark upon in order to get the greatest return for least input.

3: Investment Appraisal Analysis

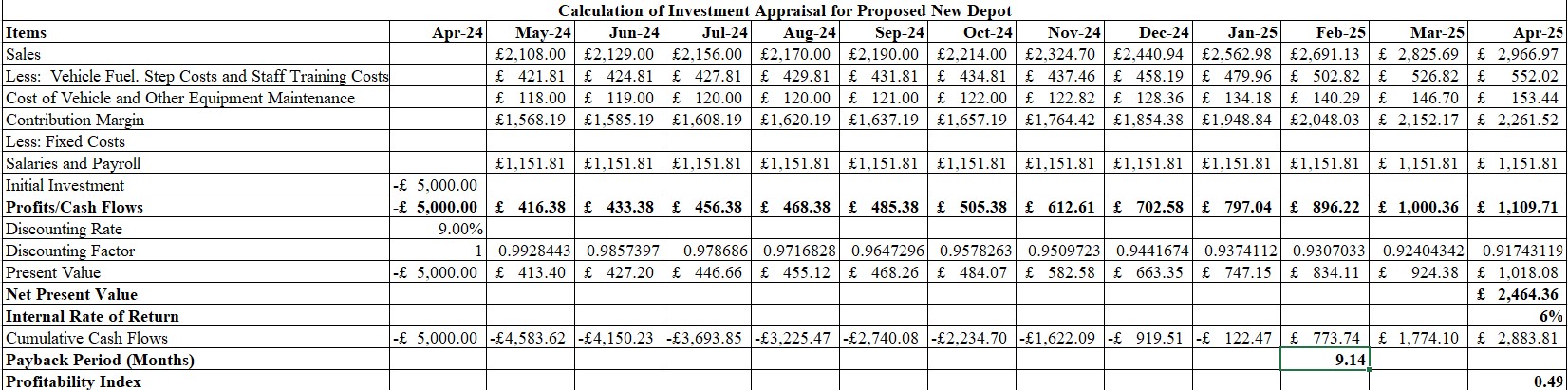

Figure 1: Calculations of Investment Appraisal

3.1: Assumptions

- The projected initial investment cost is considered as GBP 5,000.

- The discounting factors will be converted into monthly figures and a monthly format of investment appraisal analysis will be conducted.

- Salaries and Payroll costs are assumed as fixed costs while vehicle fuel, step costs, staff training costs as well as cost of vehicle and other equipment maintenance costs are identified as variable by nature.

- The methods of investment appraisal that will be evaluated are net present value, internal rate of return, payback period and profitability index.

3.2: Net Present Value

From the above figure of calculations, the net present value (NPV) has been calculated as GBP 2464.36 for CCL. The identified NPV value is deemed positive and hence project selection criteria are met by CCL if NPV is given utmost priority. Yan & Zhang (2022), illustrated and narrated that a positive NPV value for an investment or project is considered beneficial for a company due to which high expected future returns can be generated to boost financial credentials.

3.3: Internal Rate of Return

As per the above pictorial demonstration of investment of appraisal calculations, internal rate of return (IRR) has been calculated as 6%. The identified figure of IRR is considered to be fractionally lower in comparison to the cost of capital projected as 9% and hence future financial complexities are likely to be suffered by CCL. Wang (2021), critically explained and stated that a low IRR in comparison to cost of capital could also symbolise high economic risks due to which financial sustainability can become jeopardised.

3.4: Payback Period

According to the above figure of calculations, the payback period (PBP) of the new proposed depot project is measured as 9.14 months. The PBP of the new depot project is identified to fall within the total lifespan of 12 months and hence the project could be selected if PBP criteria is given top-most selection priority.

3.5: Profitability Index

Based on the above identified figures of investment appraisal calculations, the profitability index (PI) for the new project is calculated as 0.49 times for CCL. The PI for the new depot project of CCL is identified to be positive and could be selected since higher profit generation opportunities exist.

4: Budgeting Approach for Clark Casc Logistics Plc

Clark Casc Logistics (CCL) is a UK based transport and logistics firm that enjoys operations in an environment characterised by high competition. In its struggle for retaining its market position and attaining the long-term organisational goals and objectives this company’s budgeting should fully take into account its operational complexity. It should help in the rational allocation of resources to increase operating effectiveness, revenues, and profits as well as the firm's ability to adapt to existing and emerging industry issues (Mauro, Cinquini & Grossi, 2020).

4.1: Integration from Top and from Bottom

CLC opted for a strategic budgeting system that would incorporate both, the strategic focus from top management and the organisational feedback from the subordinates. Top-down approach maintains corporate strategic direction in preparing the operational business schedule while the bottom-up approach captures the actual business needs of the ground operations, demand forecasts, fuel costs and labor needs (Imperial, 2021).

4.2: Activity Based Budgeting (ABB)

This system gives an insight on why Activity-Based Budgeting is appropriate for logistics. Therefore, by pointing out definite cost controlling factors like vehicle maintenance, fuel, and warehousing costs, Clark Casc can easily manage resources pertaining to it. ABB offers enhanced cost estimation of certain services or certain routes thereby enhancing decision making.

4.3: Rolling Budgets

Because of these, it is suggested that CCL should embrace the use of the rolling budgets because logistics is often characterised by a high degree of dynamism. When budgets are set quarterly or on a monthly basis the company can make some corrections depending on the current fuel prices or the demand throughout the year.

4.4: Scenario Planning

Since the problem involves uncertainties, the company should embrace the scenario of planning on budget. Thus, by running some eventualities such as the economic downturn or lack of supply chain, CCL can create back up plans and establish reserves.

4.5: The Performance Observation and Metrics

Budgeting must be tied to such an activity-based cost as cost per mile, delivery time and satisfactory level of customers. Recurring evaluations also offer checks and balances functions together with constant improvement.

Using this approach to structured and flexible budgeting meant that the CCL can have a strong grip over its financial determinants while retaining the flexibility required to operate amidst cut throat competition.

5: Budgeting Calculations and Analysis

5.1: Assumptions

- The growth rate of monthly sales from November 2024 to April 2025 is assumed as 5%.

- Vehicle fuel growth rate from November 2024 to April 2025 is assumed as 0.64% which is the average growth rate realised from May to October 2024.

- The preparation of an income and expenditure budget is considered to be carried out by conducting a quarterly analysis.

5.2: Sales Budget

Figure 2: Sales Budget

From the above figure of sales budget, the total sales value expected to be generated is calculated as GBP 28779.41 (000). The trend of sales budget is considered to be increasing gradually every month which is identified as a positive sign for CCL to encourage operational scalability and mobility in future. As per explanations and illustrations of Homauni et al. (2023), the sales budget is identified as a critical tool of measuring financial performances which considers projections and future speculations that a company aims to target for meeting financial objectives. The highest monthly sales value figure identified is calculated as GBP 2966.97 in April 2025.

5.3: Salaries and Payroll Cost Budget

Figure 3: Salaries and Payroll Cost Budget

According to the above figure of salaries and payroll cost budget a total figure of GBP 11309.88 is identified for CCL. The total salaries and payroll costs dispatched by CCL excluding superannuation, contribution to ENIC and bonus is calculated as GBP 9210. The total salaries and payroll costs offered to heavy goods vehicle drivers, refrigerated goods depot operatives and administrative staff salaries are individually calculated as GBP 7070, 1843 and 297 respectively. Based on the above analysis it is depicted that the proportion of salaries to heavy goods vehicle drivers is significantly higher in comparison to salaries of depot operatives and administrative staff. Du et al. (2023), critically stated and illustrated that a high proportion of labour and salary costs can become a challenging proposition for an organisation due to which reduction in profitability is expected. The salaries and payroll cost budget are also essential on part of an organisation to project future labour targets in order to generate more employment opportunities and consequently improve business operating levels.

Business economics assignments in a global finance context demand multi-layered analysis; students regularly turn to finance assignment help to navigate international market theories and economic frameworks accurately.

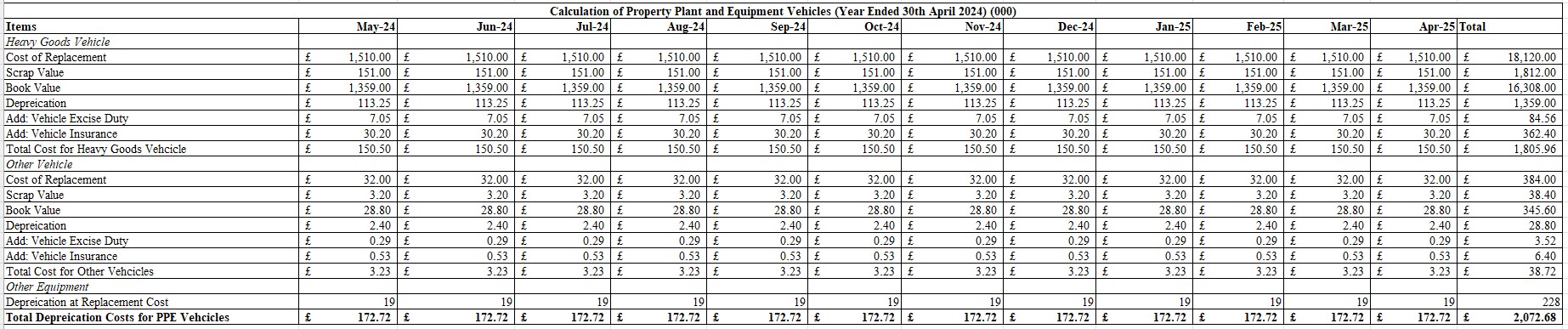

5.4: Property, Plant and Equipment Budget

Figure 4: Property, Plant and Equipment Budget

From the above calculations of total depreciation cost for property, plant and equipment vehicles, and numerical value of GBP 2072.68 is recognised for CCL. The individual depreciation for heavy vehicles is calculated as GBP 1359 and the depreciation for other vehicles and other equipment is calculated as GBP 28.80 and 228 respectively. Hence, it can be identified that a higher proportion of depreciation is paid in favour of heavy goods vehicles in comparison to other equipment and vehicles. The consideration of depreciation is a reliable method that is applied by organisations which takes into account actual book value factoring after excluding wear and tear (Sitinjak et al. 2023).

5.5: Building Depreciation and Maintenance Budget

Figure 5: Building Depreciation and Maintenance Budget

From the above figure of building depreciation and maintenance budget, total costs budgeted to be paid by CCL is identified as GBP 3234 till April 30 2025. The building depreciation cost is individually calculated as GBP 3150 while average maintenance cost expected to be paid annually is calculated as GBP 84. On the basis of the above analysis, building depreciation quantum is significantly superior in comparison to annual maintenance cost volume. As critically explained and idealised by Groenewald et al. (2024), a high value of building appreciation is considered adverse since this scope of maximising asset and net worth value becomes limited on part of an organisation.

5.6: Vehicle Cost and Other Equipment Budget

Figure 6: Vehicle Cost and Other Equipment Budget

From the above figure of vehicle cost and other equipment budget, total cost paid by CCL is measured as GBP 1545.78. The total value of other equipment cost is further measured as GBP 144. Based on the above analysis, it can be established that a relatively lower figure of vehicular costs and equipment is facilitated by CCL to create and develop future financial budgeting. As per expressions and opinions of Aidi, Ali & Flayyih (2023), a low value of vehicle cost and other equipment budget is deemed favourable for an organisation which initiates prospects of cost savings that could promote future profit maximisation.

5.7: Vehicle Fuel, Staff Training and Step Fixed Cost Budget

Figure 7: Vehicle Fuel, Staff Training and Step Fixed Cost Budget

From the above figure of calculations, total vehicle fuel, staff training and step fixed cost budget indicates numerical expressions of GBP 458.19 from May 2024 to April 2025. The individual figures of total vehicle fuel costs, staff training costs and total step fixed costs are further calculated as GBP 450.38, GBP 1.73 and GBP 6.08 respectively. Based on the above analysis, it is depicted that a high proportion of vehicular fuel costs is paid by CCL in comparison to staff training and step fixed costs. As per opinions and explanations of Uysal, Li & Mulvey (2024), a high vehicle fuel cost is indicative of a company increasing its business operations and sales due which allows better scope and prospects of magnifying market reach.

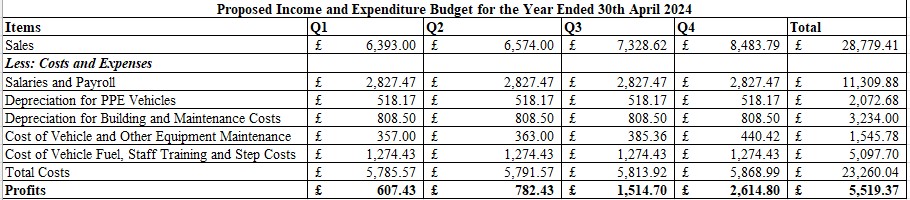

5.8: Proposed Income and Expenditure Budget

Figure 8: Proposed Income and Expenditure Budget

From the above figure of proposed income and expenditure budget, total profits for CCL have been calculated as GBP 5519.37. The profits earned from quarters 1 to 4 are calculated as GBP 607.43, 782.43, 1514.70 and 2614.80. Based on the above analysis, it can be identified that the profit quantum for CCL is witnessing an increasing trend in recent times. The increase in profit trends is mainly attributed to growth recognised for sales values. Bella, Apriyanti & Sriwijayanti (2023), illustrated and stated that growth in profits is considered as a beneficial prospect for an organisation due to which future business stability and improvements in budgeting can be contemplated.

6: Conclusion

Clark Casc Logistics Plc effectively utilises strong financial and budgetary strategies to enhance decision making of the company as well as the distribution of its resources. With the help of NPV, IRR, PBP, PI, the company assesses investment opportunities to achieve maximum profit and increase its value. Its budgeting combines both the centralised and decentralised approach, uses the rolling budgets and considers the use of scenarios and metrics. This well-disciplined but not rigid managing approach guarantees financial predictability, operational organisation, and elastically makes CCL prepared for continuous successes in a rather uncompromising logistics market.

The investment appraisal analysis section in this report illustrates the fact that a positive NPV is expected by CCL if another depot is opened within the next 12 months. However, the project is also identified to carry economic risks as the IRR identified is lower in comparison to the project cost of capital. The budgeting analysis section in this report has exclusively illustrated that profit growth is anticipated in recent times by CCL wherein the company has the ability to manage and prevent maximisation of variable and fixed costs.

7: Recommendations

Based on the above investment appraisal and budgeting analysis, the opening of a new depot by CCL should be accepted with immediate effect. This recommendation is justified on the back of locating a positive NPV value and by identifying the project payback period within 12 months as well as the scope of obtaining a positive profitability index. Further recommendations offered to the managerial concern of CCL include identification of additional revenue streams in order to boost future scope and opportunity of profit maximisation and growth.

References

- Aidi, I. S., Ali, Z. N., & Flayyih, H. H. (2023). Is It Possible To Adopt A Budget Of Performance In The Iraqi Government Companies?. International Journal of Professional Business Review: Int. J. Prof. Bus. Rev., 8(5), 63.https://dialnet.unirioja.es/servlet/articulo?codigo=8956996

- Alsharari, N. M. (2020). Accounting changes and beyond budgeting principles (BBP) in the public sector: Institutional isomorphism. International Journal of Public Sector Management, 33(2/3), 165-189. https://www.emerald.com/insight/content/doi/10.1108/IJPSM-10-2018-0217/full/html

- Baum, A. E., Crosby, N., & Devaney, S. (2021). Property investment appraisal. John Wiley & Sons. https://books.google.com/books?hl=en&lr=&id=4-ASEAAAQBAJ&oi=fnd&pg=PP1&dq=Investment+Appraisal+Approach+&ots=GMUwXkhZhS&sig=DQWVzUJSGnUTTcrJEzAJygxx36c

- Bella, S., Apriyanti, N., & Sriwijayanti, H. (2023). Enhancing financial management and accountant roles: A study on the role of technological advancements. SEIKO: Journal of Management & Business, 6(2), 435-446.https://www.journal.stieamkop.ac.id/index.php/seiko/article/view/4842

- Du, X., Xi, M., Kong, L., Chen, X., Zhang, L., Zhang, H., ... & Wu, W. (2023). Energy budgeting and carbon footprint of different wheat–rice cropping systems in China. Science of The Total Environment, 879, 163102.https://www.sciencedirect.com/science/article/pii/S0048969723017217

- Groenewald, E., Rabillas, A., Uy, F., Kilag, O. K., Bugtai, G., & Batilaran, J. (2024). Enhancing Financial Management Practices in Public Schools: A Systematic Literature Review in Southeast Asia. International Multidisciplinary Journal of Research for Innovation, Sustainability, and Excellence (IMJRISE), 1(2), 207-212.https://www.researchgate.net/profile/Elma-Groenewald-2/publication/378508162_Enhancing_Financial_Management_Practices_in_Public_Schools_A_Systematic_Literature_Review_in_Southeast_Asia/links/65dddbb9c3b52a1170fbfea8/Enhancing-Financial-Management-Practices-in-Public-Schools-A-Systematic-Literature-Review-in-Southeast-Asia.pdf

- Homauni, A., Markazi-Moghaddam, N., Mosadeghkhah, A., Noori, M., Abbasiyan, K., & Jame, S. Z. B. (2023). Budgeting in healthcare systems and organizations: a systematic review. Iranian Journal of Public Health, 52(9), 1889.https://www.ncbi.nlm.nih.gov/pmc/articles/PMC10682572/

- Imperial, M. T. (2021). Implementation structures: The use of top-down and bottom-up approaches to policy implementation. In Oxford research encyclopedia of politics. https://oxfordre.com/politics/display/10.1093/acrefore/9780190228637.001.0001/acrefore-9780190228637-e-1750;!!IKRxdwAv5BmarQ!YkEBWJ1--fpzkjVAUx8a8gqQ9qUFNuUMsWSq-VoZ5UEn-cA5mBDluWgWuSONnNlLk2E2RCUI4hrtqcvE1jM$

- Imteaz, M. A., Bayatvarkeshi, M., & Karim, M. R. (2021). Developing generalised equation for the calculation of payback period for rainwater harvesting systems. Sustainability, 13(8), 4266. https://www.mdpi.com/2071-1050/13/8/4266

- Mauro, S. G., Cinquini, L., & Grossi, G. (2020). Insights into performance-based budgeting in the public sector: a literature review and a research agenda. Public Budgeting in Search for an Identity, 7-27. https://www.taylorfrancis.com/chapters/edit/10.4324/9781003133575-2/insights-performance-based-budgeting-public-sector-literature-review-research-agenda-sara-giovanna-mauro-lino-cinquini-giuseppe-grossi

- Peymankar, M., Davari, M., & Ranjbar, M. (2021). Maximizing the expected net present value in a project with uncertain cash flows. European Journal of Operational Research, 294(2), 442-452. https://www.sciencedirect.com/science/article/pii/S0377221721000692

- Sitinjak, C., Johanna, A., Avinash, B., & Bevoor, B. (2023). Financial Management: A System of Relations for Optimizing Enterprise Finances–a Review. Journal Markcount Finance, 1(3), 160-170.https://journal.ypidathu.or.id/index.php/jmf/article/view/104

- Uysal, A. S., Li, X., & Mulvey, J. M. (2024). End-to-end risk budgeting portfolio optimization with neural networks. Annals of Operations Research, 339(1), 397-426.https://link.springer.com/article/10.1007/s10479-023-05539-4

- Wang, Y. (2021, December). The development and usage of NPV and IRR and their comparison. In 2021 3rd International Conference on Economic Management and Cultural Industry (ICEMCI 2021) (pp. 2044-2048). Atlantis Press.https://www.atlantis-press.com/proceedings/icemci-21/125966320

- Yan, R., & Zhang, Y. (2022, March). The Introduction of NPV and IRR. In 2022 7th International Conference on Financial Innovation and Economic Development (ICFIED 2022) (pp. 1472-1476). Atlantis Press.https://www.atlantis-press.com/proceedings/icfied-22/125971692